What if you wanted to forecast a 10% increase in sales for next year across all product lines? This is where scalar multiplication comes in. A scalar is just a fancy word for a single number. Multiplying a vector by a scalar applies that number to every element in the vector. The following code applies the 10% to the 2024 numbers:

import numpy as np

# Scale 2024 sales by 10%

q_2024 = np.array([100, 200, 150])

scaled_q = 1.1 * q_2024

print(scaled_q)

The result, [110. 220. 165.], shows the effect of forecasting a 10% increase in all product sales.

Every entry in the vector grows proportionally.

The Dot Product

The dot product is one of the most important operations in all of linear algebra, especially in business. It works by multiplying the corresponding elements of two vectors and then summing the results.

p ⋅ q = p 1 q 1 + ⋯ + p n q n In plain language, the dot product measures how much two vectors “line up” with each other. In business, it often means combining prices and quantities to compute revenue, or portfolio weights and asset returns to compute overall return. In Python, the dot product is handled by NumPy’s np.dot function. In the following code snippet, you can compute total revenue by finding the dot product between the prices and the q_2024 vectors.

import numpy as np

# Total revenue in 2024

q_2024 = np.array([100, 200, 150])

prices = np.array([5, 10, 15])

revenue_2024 = np.dot(prices, q_2024)

print(revenue_2024)

The dot product executed the calculation (5 × 100) + (10 × 200) + (15 × 150) in a single, optimized step. The result, 4750, is the total revenue for 2024. This operation is fundamental for everything from calculating portfolio returns to machine learning.

64 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

Norms (Vector Lengths)

The norm of a vector measures its size or magnitude. Think of it as the distance from the origin to the point represented by the vector. In business, norms can help measure total exposure, intensity of demand, or even compare the “scale” of different operations.

While there are several ways to calculate a vector’s “size,” the most common and intuitive method is the Euclidean norm, also known as the L2 norm. This is exactly what it sounds like: it calculates the straight-line distance from the origin (0, 0, 0) to the vector’s point in space. It’s a direct, multi-dimensional application of the Pythagorean theorem. To calculate this in Python, you use the norm function, which is located inside NumPy’s linear algebra submodule, linalg. This is a sub-package within the NumPy library in Python, providing a set of functions for performing linear algebra operations.

Using the simple helper function, you can compute the norm with the following code snippet: import numpy as np

# Calculate the magnitude of the 2024 sales vector

q_2024 = np.array([100, 200, 150])sales_norm_2024 =

np.linalg.norm(q_2024)print(sales_norm_2024)

The result of this code is 269.258. The np.linalg.norm function is performing a calculation you’re already familiar with from the dot product. It’s effectively squaring every element in the vector (100**2 + 200**2 + 150**2), summing them, and then taking the square root. This is similar to the Pythagorean theorem. In fact, this is directly related to the dot product: the dot product of a vector with itself (e.g., np.dot(q_2024, q_2024)) gives you the squared norm (72500). The result from this code snippet is the square root of that number. While this number is more abstract than total revenue, it gives you a single metric to summarize the vector’s size, which is incredibly useful for more advanced comparisons and algorithms.

Combining Matrices

So far, you’ve learned about vectors, but what if you have two years’ worth of sales data? You need a simple way to combine these into a single variable to make your analysis easier, allowing you to perform operations on multiple years at once. This is where matrices come in.

To build the sales matrix, you start, as always, with NumPy and the two sales vectors. You need a way to combine them, and the np.column_stack function is designed for exactly this. You give this function your list of vectors, [q_2024, q_2025], and it neatly stacks them side-by-side, turning each vector into a vertical column in the new 2D matrix, Total_Quantity. Consider the following example, which builds a sales matrix where each column is a year:

import numpy as np

# Sales quantities (vectors)

q_2024 = np.array([100, 200, 150])

q_2025 = np.array([120, 210, 160])

Total_Quantity= np.column_stack([q_2024, q_2025])

print(Q)

operations with Vectors and Matrices ❘ 65

Just like in the previous examples, you start with your toolkit, numpy, and the two vectors of sales quantities. You need a way to combine everything into one matrix. This is where np.column_stack comes in. You give this function your list of vectors, [q_2024, q_2025], and it neatly stacks them side-by-side, turning each vector into a vertical column in a new 2D matrix. The np.column_stack function can work with 1D vectors or 2D matrices. This new, combined table is stored in the variable Q. Finally, if you call print(Q), you see this result:

100 120

200 210

[150 160]

Now your data is in one place. You can clearly see that the rows represent the three products (at indices 0, 1, and 2), and the columns represent the years (2024 at index 0 and 2025 at index 1). This organized structure is much more powerful. You can now access all of 2024’s data by simply grabbing the first column or see the full history for the second product by grabbing the second row.

Slicing Matrices

A matrix is a fantastic way to store a complete dataset, such as the sales performance for all your products across all your regions. But in real-world analysis, you’ll rarely work with the entire matrix at once. More often, you’ll want to isolate a specific piece of it. For example, what if you want to retrieve only 2024 sales again? This process of grabbing specific parts of your matrix is called slicing.

NumPy uses a powerful and intuitive bracket notation, matrix[row_selector, column_selector], to select data. The key thing to remember is that, like all of Python, NumPy is zero-indexed, meaning the first row is at index 0, the second at index 1, and so on.

Let’s begin with the stacked sales_data matrix from the previous example. This contains the sales vectors from 2024 and 2025.

import numpy as np

# Sales quantities (vectors) for 3 products

q_2024 = np.array([100, 200, 150])

q_2025 = np.array([120, 210, 160])

# Stack the vectors as columns

Q = np.column_stack([q_2024, q_2025])

print("--- Sales Matrix (Q) ---")

print(Q)

Again, NumPy uses an intuitive bracket notation to select data.

matrix[row_selector, column_selector]

66 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

To get a single value, you simply provide its coordinates. For example, to find the sales for “Product 1” (row 1) in “2025” (column 1), you would use Q[1, 1], which would return 210.

The real power comes from using the colon (:) as a wildcard, which means “select all.” If you want to get the entire sales history for “Product 0” (row 0), you ask for row 0 and all columns. The syntax for this is Q[0,:]. This returns the full vector [100, 120], which you can then analyze or plot.

This works the same way for columns. To isolate the sales for all products in just “2024” (column 0), you would use Q[:, 0]. This would give you the vector [100, 200, 150], which is the original q_2024

vector. This ability to instantly pull out a single year’s data or a single product’s history is a fundamental part of daily data analysis. Mastering this [row, column] slicing is the key to moving from looking at a whole dataset to surgically extracting the exact insights you need.

Matrix Multiplication

There are many cases where you want to multiply a matrix by another, or perform matrix multiplication. When you multiply a price vector by the sales matrix, you compute revenue for multiple years at once. The following example multiplies the prices vector by the Q sales matrix: import numpy as np

# Sales quantities (vectors)

q_2024 = np.array([100, 200, 150])

q_2025 = np.array([120, 210, 160])

Q = np.column_stack([q_2024, q_2025])

prices = np.array([5, 10, 15])

# Revenue for 2024 and 2025

revenues = prices @ Q

print(revenues)

Running this snippet produces the following result:

[4750 5100]

What did the @ operator actually do? It took the prices vector and performed a dot product against every single column of the Q matrix. With one simple operation, you calculated the total revenue for 2024 ($4,750) and 2025 ($5,020). Note the following:

➤

The first element (4750): This is the result of np.dot(prices, q_2024), which is (5 × 100)

+ (10 × 200) + (15 × 150).

➤

The second element (5020): This is the result of np.dot(prices, q_2025), which is (5 × 120) + (10 × 210) + (15 × 160).

This ability to perform operations on entire datasets at once is why linear algebra is the backbone of data science and analytics. Instead of writing a for loop to calculate revenue for each year, you can express your problem as a single matrix operation. This ability to perform batch operations on entire datasets at once makes the code faster, cleaner, and more powerful.

Creating and Manipulating Vectors (and Matrices) with numPy ❘ 67

Transpose

The transpose flips rows into columns and columns into rows. Sometimes you’ll want to change perspective: from “sales by product across years” to “sales by year across products.” That can be done by simply using the transpose attribute on a matrix, which is done by adding .T, as shown here: import numpy as np

# Sales quantities (vectors) for 3 products

q_2024 = np.array([100, 200, 150])

q_2025 = np.array([120, 210, 160])

# Stack the vectors as columns

Q = np.column_stack([q_2024, q_2025])

print(Q.T)

The result is as follows:

[

100 200 150

120 210 160]

Transposing a matrix is rotating the data, making it easier to view from different perspectives. But it can also be important for mathematical operations later.

Linear algebra is powerful because it mirrors the way businesses already think, but with the precision and efficiency of mathematics. With Python, these operations are not abstract ideas but real, computable processes that managers, analysts, and students can run instantly.

CREATING AND MANIPULATING VECTORS (AND MATRICES)

WITH NUMPY

Let’s put these linear algebra skills to the test with a classic finance problem: creating and tracking a stock portfolio. You’ll use NumPy to see how these concepts make complex financial analysis surprisingly straightforward.

The goal is to model a portfolio of three stocks over a six-day period. You will: 1.

Start with a matrix of historical prices.

2.

Calculate a matrix of daily stock returns from those prices.

3.

Test two different investment strategies by combining the returns with weight vectors.

68 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

The two strategies you’ll compare are as follows:

➤

A constant-weight “set-it-and-forget-it” approach.

➤

A time-varying approach that actively rebalances the portfolio daily.

First, you need data to work with. This example creates a price matrix called stock_prices for three fictional stocks (“A”, “B”, and “C”) over six trading days. In this matrix, each row will represent a day, and each column will represent a stock. This arrangement, often described by its “shape”

(number of rows, number of columns), is a standard convention in financial analysis. Listing 4-l sets up all the initial data: the stock tickers, the dates, and the stock_prices matrix.

LISTING 4-1: SETTING UP THE DATA

import numpy as np

# Setup: tickers, dates, and a small price matrix

tickers = np.array(["A", "B", "C"])

dates = np.array(["2025-01-02","2025-01-03","2025-01-06","2025-01-07","2025-01-08","2025-01-09"])

# Price matrix: rows are dates, columns are assets

# A B C

stock_prices = np.array([

[100., 50., 25.],

[101., 49., 25.5],

[102., 48., 26.0],

[101., 48.5, 25.8],

[103., 49., 25.9],

[104., 50., 26.2]

])

# Get the dimensions of the matrix using the .shape attribute

# .shape returns a tuple: (number_of_rows, number_of_columns)

num_time_periods, num_assets = stock_prices.shape

print("Prices matrix shape:", stock_prices.shape)

print(f" (This means {num_time_periods} time periods and {num_assets} assets)") print("Assets:", tickers)

print("Dates:", dates)

The result of the setup is a matrix, P, of stock returns, with asset names and dates: Prices matrix shape: (6, 3)

Assets: ['A' 'B' 'C']

Dates: ['2025-01-02' '2025-01-03' '2025-01-06' '2025-01-07' '2025-01-08'

'2025-01-09']

Running this code block sets up your environment. The first output line, Prices matrix shape: (6, 3), confirms the dimensions of the stock_prices matrix. The .shape function gives you the dimensions of a matrix. This is a key check: as you can see from the new print statement, you have six rows (the num_time_periods) and three columns (the num_assets), just as designed.

Creating and Manipulating Vectors (and Matrices) with numPy ❘ 69

The subsequent lines print the asset tickers and the corresponding dates. With the raw price data now loaded into a clean NumPy matrix, you are ready to begin the analysis and calculate the daily returns.

Step 1: Compute Asset Returns from Prices

A stock’s price is just a number; its performance is measured by its return. For analysis, you’ll calculate the simple daily return, which answers the question, “What was the percentage change from yesterday to today?” The formula is as follows:

(today's price / yesterday's price) - 1

You could, of course, write a for loop to iterate over every day and every stock to calculate this, but NumPy gives you a much more powerful and elegant way to do this for all stocks and all days in a single line. This is done using a feature called broadcasting.

Broadcasting is NumPy’s function for performing arithmetic operations on arrays of different shapes.

It “stretches” the smaller array to match the shape of the larger one without the overhead of actually copying the data. You can use a bit of array slicing to make this work. If you want to divide today’s prices by yesterday’s prices, you can create two new matrices from the stock_prices matrix: one that represents today and one that represents yesterday. stock_prices[1:] is a slice of the price matrix stock_prices containing all rows from the second day to the end. This will be your today’s price matrix. stock_prices[:-1] is a slice containing all rows from the first day up to (but not including) the last day. This will be your yesterday’s price matrix.

Because these two new matrices have the exact same shape (five rows and three columns), NumPy can perform element-wise division on them instantly. As shown in Listing 4-2, you then subtract 1

to get the final return. The resulting matrix, named Returns, will naturally have one fewer row than your original stock_prices matrix, because returns only occur between days.

LISTING 4-2: PERFORMING ELEMENT-WISE DIVISION

import numpy as np

stock_prices = np.array([

[100., 50., 25.],

[101., 49., 25.5],

[102., 48., 26.0],

[101., 48.5, 25.8],

[103., 49., 25.9],

[104., 50., 26.2]

])

returns = stock_prices[1:] / stock_prices[:-1] - 1

Now, each row of R is a vector of asset returns for that period. This is exactly the “vectors of numbers” view you want: a period’s returns are just a return vector. Stack those vectors, and you have a return matrix.

To see how the three stocks performed, you can import the pyplot library from Matplotlib and create a simple visualization of your new returns matrix, returns. This is shown in Listing 4-3.

70 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

LISTING 4-3: SEEING HOW THE THREE STOCKS PERFORMED

import matplotlib.pyplot as plt

import numpy as np

stock_prices = np.array([

[100., 50., 25.],

[101., 49., 25.5],

[102., 48., 26.0],

[101., 48.5, 25.8],

[103., 49., 25.9],

[104., 50., 26.2]

])

returns = stock_prices[1:] / stock_prices[:-1] - 1

plt.plot(R)

plt.show()

Step 2: Portfolio with Constant Weights

The first strategy for your financial problem is simple: you allocate your money at the start and never change it. This is the “set-it-and-forget-it” approach.

To model this, this example creates a weight vector called weight that assigns 50% of your portfolio to Stock A, 30% to B, and 20% to C. To find the portfolio’s total return on any given day, you just need to calculate the dot product of that day’s return vector (a row from returns) and your w vector.

0.020

0.015

0.010

0.005

0.000

–0.005

–0.010

–0.015

–0.020

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FIGURE 4-1: A simple plot showing stock returns over time.

Creating and Manipulating Vectors (and Matrices) with numPy ❘ 71

Thanks to NumPy, you can calculate the entire time series of portfolio returns in one shot using matrix-vector multiplication, returns @ weights. Listing 4-4 shows the full listing of this solution.

LISTING 4-4: CALCULATING WITH MATRIX-VECTOR MULTIPLICATION

import numpy as np

stock_prices = np.array([

[100., 50., 25.],

[101., 49., 25.5],

[102., 48., 26.0],

[101., 48.5, 25.8],

[103., 49., 25.9],

[104., 50., 26.2]

])

returns = stock_prices[1:] / stock_prices[:-1] - 1

# Constant weights for our three stocks (must sum to 1)

weights = np.array([0.5, 0.3, 0.2])

# Calculate the portfolio's return for every single day

# This is matrix-vector multiplication: (5, 3) @ (3,) -> (5,)

r_p_const = returns @ weights

# Let's see how $1 invested at the start would have grown

# We need to calculate the cumulative product of the daily growth

portfolio_index_const = np.cumprod(1 + r_p_const)

print("Ending portfolio value (constant weights):", portfolio_index_const[-1]) The returns @ weights operation efficiently computes the portfolio’s performance over time. This is the same math as (weight_A × return_A) + (weight_B × return_B) + ⋯ , repeated for every day. The resulting portfolio value with constant weights is 1.029.

To track the growth of a $1 investment, you use the np.cumprod function. This is a powerful tool for calculating a cumulative product. It takes your series of daily returns (e.g., [1.003, 1.002, 0.999]) and calculates the compounding growth: [1.003, (1.003 × 1.002), (1.003 × 1.002 × 0.999)]. This gives the index value for each day. You can also visualize the portfolio value over time using the code in Listing 4-5.

LISTING 4-5: VISUALIZING THE PORTFOLIO VALUE OVER TIME

import numpy as np

import matplotlib.pyplot as plt

stock_prices = np.array([

[100., 50., 25.],

[101., 49., 25.5],

[102., 48., 26.0],

[101., 48.5, 25.8],

72 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

[103., 49., 25.9],

[104., 50., 26.2]

])

returns = stock_prices[1:] / stock_prices[:-1] - 1

# Constant weights for our three stocks (must sum to 1)

weights = np.array([0.5, 0.3, 0.2])

# Calculate the portfolio's return for every single day

# This is matrix-vector multiplication: (5, 3) @ (3,) -> (5,)

r_p_const = returns @ weights

# Let's see how $1 invested at the start would have grown

# We need to calculate the cumulative product of the daily growth

portfolio_index_const = np.cumprod(1 + r_p_const)

plt.plot(portfolio_index_const)

plt.show()

Step 3: Portfolio with Time-varying Weights

Most serious strategies involve periodic rebalancing. The “set-it-and-forget-it” model was simple, but this step models a simple active strategy. Instead of a single weight vector, you will create a weight matrix (called WEIGHTS), where each row represents a different weight vector for each day.

1.030

1.025

1.020

1.015

1.010

1.005

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FIGURE 4-2: A simple line plot showing portfolio value over time.

Creating and Manipulating Vectors (and Matrices) with numPy ❘ 73

The simple rule: each day, you’ll slightly increase your investment in whichever stock performed best the day before.

To set this up, you first create a 5 × 3 W matrix by “tiling” the constant weights vector. To do this, you use np.tile, which is a function that repeats an array. This function is a “tiling” utility: it takes an array and repeats it. You’re telling NumPy to take your weights vector and tile it five times vertically (returns.shape[0]) and one time horizontally, producing a 5 × 3 matrix of the starting weights.

Then, you’ll loop from the second day onward. Inside the loop, you use np.argmax to find the index (0, 1, or 2) of yesterday’s (t − 1) winning stock. You then nudge the weight for that winner up by 0.05

and re-normalize the row so all weights sum back to 1. This is all shown in Listing 4-6.

LISTING 4-6: USING A WEIGHT MATRIX

import numpy as np

import matplotlib.pyplot as plt

stock_prices = np.array([

[100., 50., 25.],

[101., 49., 25.5],

[102., 48., 26.0],

[101., 48.5, 25.8],

[103., 49., 25.9],

[104., 50., 26.2]

])

returns = stock_prices[1:] / stock_prices[:-1] - 1

# Constant weights for our three stocks (must sum to 1)

weights = np.array([0.5, 0.3, 0.2])

# Start with our constant weights as a baseline

WEIGHTS = np.tile(weights, (returns.shape[0], 1))

# A simple rebalancing rule:

for t in range(1, returns.shape[0]):

# Find the index of yesterday's winning stock

winner_idx = np.argmax(returns[t-1])

# Nudge the weight for today's portfolio toward that winner

WEIGHTS[t, winner_idx] += 0.05

# Re-normalize the row to ensure weights sum back to 1

WEIGHTS[t] = WEIGHTS[t] / WEIGHTS[t].sum()

# Calculate time-varying portfolio returns

# This is a row-by-row dot product: (Day 1 returns * Day 1 weights) + ...

r_p_timevary = np.sum(returns * WEIGHTS , axis=1)

portfolio_index_timevary = np.cumprod(1 + r_p_timevary)

print("Ending portfolio value (time-varying weights):", portfolio_index_timevary[-1])

74 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

The for loop—for t in range(1, returns.shape[0]):—is where the new logic lives. Notice that it starts at 1 (the second day), not 0, because this rule depends on yesterday’s (t-1) performance.

Inside the loop, the first line is winner_idx = np.argmax(returns[t-1]). The np.argmax function is a new and incredibly useful tool. It doesn’t return the highest value from the array; instead, it returns the index (0, 1, or 2) of that highest value. This is exactly what you need. You’re asking it,

“For yesterday’s returns, which stock won?” This returns 0 (for Stock A), 1 (for Stock B), or 2 (for Stock C).

The next line, WEIGHTS[t, winner_idx] += 0.05, uses that index. It’s a precise update: “Go to the WEIGHTS matrix, find the row for today (t), and in that row, find the column for winner_idx and add 0.05 to its weight.”

Of course, this means your weights for that day no longer add up to 1. That’s why the final line in the loop, WEIGHTS[t] = WEIGHTS[t] / WEIGHTS[t].sum(), is so critical. It’s a “re-normalization”

step. It calculates the new sum of the row and then divides the entire row by that sum. This scales all weights back down, ensuring they once again add up to 1.

After the loop is finished, you have your WEIGHTS matrix, where each row is a slightly different portfolio allocation. The r_p_timevary = np.sum(returns * WEIGHTS, axis=1) line is the NumPy way of performing a row-by-row dot product. The returns * WEIGHTS operation performs an element-wise multiplication, and np.sum(..., axis=1) then sums those products horizontally, giving the total portfolio return for each specific day. Finally, you can use np.cumprod just as before to compute the compounded growth of 1.03. You can also visualize the results with a plot, as shown

1.030

1.025

1.020

1.015

1.010

1.005

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FIGURE 4-3: A line plot showing the results of using time-varying weights.

Creating and Manipulating Vectors (and Matrices) with numPy ❘ 75

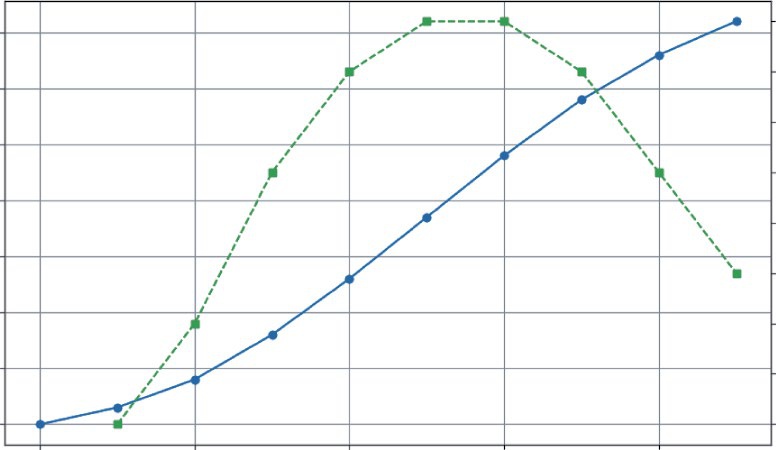

Comparing Strategies (Same Math, Different Inputs)

Because you used the same linear algebra framework for both the constant weights strategy as well as for time-varying weights strategy, the final results are two clean vectors that you can easily compare. Consider for example how an initial $1 investment would have performed with each strategy side-by-side.

Listing 4-7 uses extra print statements to display the results in a visual manner. You’ll use the enumerate function in the loop. enumerate is a helpful Python function that returns two things at once: the index number (i) and the item from the list (date). This enables you to use i to access your portfolio data while using date to print the corresponding date. Before running Listing 4-7, run the code from Listing 4-6 (it defines the data you will use for the visualization).

LISTING 4-7: EXTRA PRINT STATEMENT TO DISPLAY RESULTS VISUALLY

### Include Listing 4.6 code here ###

import numpy as np

import matplotlib.pyplot as plt

print("--- Performance Comparison (Index Value) ---")

print("Date | Constant | Time-Varying")

print("------------------------------------------")

for i, date in enumerate(dates[1:]):

const_val = portfolio_index_const[i]

timevary_val = portfolio_index_timevary[i]

print(f"{date} | {const_val:.4f} | {timevary_val:.4f}")

plt.plot(portfolio_index_const, label="Constant")

plt.plot(portfolio_index_timevary, label="Time-Varying")

plt.legend()

plt.show()

--- Performance Comparison (Index Value) ---

Date | Constant | Time-Varying

------------------------------------------

2025-01-03 | 1.0030 | 1.0030

2025-01-06 | 1.0058 | 1.0066

2025-01-07 | 1.0024 | 1.0030

2025-01-08 | 1.0162 | 1.0167

2025-01-09 | 1.0297 | 1.0300

Notice how the same core operations—dot products and matrix multiplications—allow you to model two distinct financial strategies. This is the beauty of linear algebra: it provides a powerful and efficient language for describing complex systems.

76 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

1.030

Constant

Time-varying

1.025

1.020

1.015

1.010

1.005

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FIGURE 4-4: Performance of both the constant and time-varying weights over time.

EIGENVALUES AND EIGENVECTORS: BUSINESS APPLICATIONS

Beyond day-to-day operations, every business system has dominant trends, stable states, and long-term tendencies. Eigenvalues and eigenvectors are the advanced tools that help you discover this hidden engine.

While the names sound complex, the idea is surprisingly intuitive. They help you answer critical questions like these:

➤

If current trends continue, where will our customer base be in a year?

➤

What is the single biggest risk factor driving our investment portfolio?

➤

Who are the most influential players in our supply chain network?

What Eigenvalues and Eigenvectors Represent

A matrix acts like a “wind machine,” applying a force that transforms vectors. When this “wind”

hits most vectors, it blows them in a completely new direction. But some special vectors, the eigenvectors, are perfectly aligned with the wind. When the wind hits them, they don’t change direction. They only get stretched, shrunk, or flipped. The factor by which they stretch or shrink is the eigenvalue.

In business, you can think of eigenvectors as the natural directions or stable trends of a system, and eigenvalues as the strength or magnitude of those trends.

Eigenvalues and Eigenvectors: Business Applications ❘ 77

Formally, for a matrix A and its eigenvector v, the relationship is as follows: A θ = λθ

Where λ (lambda) is the eigenvalue.

Why Eigenvalues Matter for Long-term Stability

Eigenvalues are crucial for understanding whether a system will grow, shrink, or stabilize over time.

Specifically, the value of the system’s dominant eigenvalue dictates its long-term behavior:

➤

If the dominant eigenvalue is greater than 1, the system grows exponentially. This could be viral marketing (good) or compounding portfolio risk (bad).

➤

If the dominant eigenvalue is less than 1, the system decays and fades away over time.

➤

If the dominant eigenvalue is exactly 1, the system converges to a stable, steady state, like a fixed market share or a predictable distribution of loyal customers.

To see this in action, you’ll see two powerful examples. First, you’ll see how an eigenvector can predict long-term customer loyalty and see if your business model has a “leaky bucket.” Second, you’ll use eigenvectors to analyze a stock portfolio and uncover the single biggest risk factor driving its volatility.

Predicting Long-term Customer Loyalty

Imagine you’re tracking your customers, who can be in one of three states: Active, Dormant, or Churned. You create a transition matrix that shows the probability of a customer moving from one state to another each month.

The business question: If you do nothing, where will all your customers eventually end up? The answer lies in the eigenvector associated with the eigenvalue of 1, which will give you the system’s steady state, which you can calculate in the code presented in Listing 4-8.

LISTING 4-8: USING AN EIGENVECTOR

import numpy as np

# A customer transition matrix

# Rows: Current State, Columns: Next State

# States: [Active, Dormant, Churned]

P = np.array([

[0.7, 0.2, 0.1],

[0.3, 0.5, 0.2],

[0.0, 0.0, 1.0]

])

78 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

# To find the steady-state for this type of problem, we use the transpose P.T

eigenvalues, eigenvectors = np.linalg.eig(P.T)

# Find the eigenvector corresponding to the eigenvalue of 1

steady_state_vector = eigenvectors[:, np.isclose(eigenvalues, 1)]

steady_state_vector = steady_state_vector[:, 0].real

steady_state_vector = steady_state_vector / steady_state_vector.sum() print("Eigenvalues:", eigenvalues)

print("Steady-State Distribution (A, D, C):", steady_state_vector) Running this code will produce the following output:

Eigenvalues: [1. 0.33542487 0.86457513]

Steady-State Distribution (A, D, C): [0. 0. 1.]

The first thing to notice is that it’s analyzing np.linalg.eig(P.T), which is the eigenvector of the transpose of the matrix. For finding the steady state of a transition matrix, the math requires you to find the “left eigenvector,” which, for the purposes here, you can get by finding the regular eigenvector of the transposed matrix. The np.linalg.eig function gives two arrays: eigenvalues and eigenvectors. The raw eigenvalues are [1., 0.5, 0.2], which confirms the system has a stable end-state because the dominant eigenvalue is exactly 1.

The next step is to find the eigenvector that corresponds to that eigenvalue of 1. The np.

isclose(eigenvalues, 1) line creates a Boolean mask ([True, False, False]) that finds the index of the eigenvalue equal to 1. You use this mask with the slicing syntax eigenvectors[:, ...]

to pull out the correct column (the eigenvector) from the eigenvectors matrix. This raw vector isn’t clean; it might be [0., 0., 0.89442719]. To make it a proper probability, you use .real to get only its real part (ignoring any tiny complex numbers from computation) and then normalize it by dividing the vector by its own sum. This scales all the numbers so they add up to 1.

The final, normalized steady_state_vector tells a stark story: [0. 0. 1.]. This means that, eventually, 0% of customers will be Active, 0% will be Dormant, and 100% will be Churned. The results from the eigenvector analysis show that you customers are a leaky bucket, which means that every customer is destined to leave.

uncovering the Biggest Risk in a stock Portfolio

In finance, an asset’s risk is not just about its own volatility, but how it moves with other assets. A covariance matrix captures this interconnected risk, showing, for example, if Stock A tends to go up when Stock B goes down. NumPy provides a simple function, called np.cov, to calculate this for you. It takes a matrix of data (where each row is a variable and each column is an observation) and returns a new matrix showing the covariance between all the variables.

By finding the eigenvalues and eigenvectors of this matrix, you can perform a simplified version of Principal Component Analysis (PCA), as shown in Listing 4-9, to answer the question: What is the single biggest source of risk driving my entire portfolio? Let’s start with a simple matrix of daily returns for three stocks. This matrix will have days as rows and stocks as columns.

Eigenvalues and Eigenvectors: Business Applications ❘ 79

LISTING 4-9: A SIMPLIFIED VERSION OF PRINCIPAL COMPONENT ANALYSIS

import numpy as np

# A simple matrix of daily returns for three stocks

# Rows = days, Columns = stocks

returns = np.array([

[0.01, 0.02, 0.015],

[0.005, 0.018, 0.010],

[-0.002,-0.015, -0.008],

[0.012, 0.020, 0.017],

])

# 1. Compute the covariance matrix

cov_matrix = np.cov(returns.T)

# 2. Get eigenvalues and eigenvectors (eigh is best for symmetric matrices) eigvals, eigvecs = np.linalg.eigh(cov_matrix)

# 3. Find the principal component (the one with the largest eigenvalue) idx = np.argmax(eigvals)

principal_eigenvalue = eigvals[idx]

principal_eigenvector = eigvecs[:, idx]

print(f"Largest Eigenvalue (Magnitude of Risk): {principal_eigenvalue:.6f}") print(f"Principal Eigenvector (The 'Market Factor'): {principal_eigenvector}") Running this code will produce the following output:

Largest Eigenvalue (Magnitude of Risk): 0.000455

Principal Eigenvector (The 'Market Factor'): [-0.27500973 -0.80216434

-0.5300019 ]

First, it used np.cov(R.T). You need to provide the transpose of your returns matrix because np.cov expects each row to be a variable and each column to be an observation.

Next is np.linalg.eigh(cov_matrix). This function is similar to np.linalg.eig, but it’s specifically designed for symmetric matrices (where the matrix is a mirror image of itself across the diagonal). A covariance matrix is always symmetric, and using eigh is often faster and more numerically stable. The output shows three eigenvalues. The np.argmax(eigvals) function found the index of the largest one, 0.000455. This largest eigenvalue represents the variance (or “strength”) of the most dominant risk factor.

The corresponding principal eigenvector is [−0.27500973 −0.80216434 −0.5300019]. This is a recipe showing how each stock is exposed to this main risk driver. Because all three values are positive, it suggests this dominant factor is a broad market risk that tends to move all three stocks in the same direction. Analysts use this technique to distill the risk of thousands of assets down to a handful of key driving factors.

80 ❘ CHAPTER 4 LinEAR ALgEBRA FoR BusinEss And FinAnCE

SUMMARY

Throughout this chapter, you have journeyed from the fundamental building blocks of data, vectors and matrices, to the profound insights offered by eigenvectors. More than just a collection of mathematical rules, you’ve discovered that linear algebra provides a powerful new lens for viewing business problems. With Python and NumPy, this chapter bridged the gap between theory and practice, turning abstract concepts into concrete solutions, such as calculating revenues, modeling portfolio performance, and even predicting the long-term stability of a system. As you move forward, see these tools not as abstract requirements, but as a core part of your analytical toolkit. The ability to structure a problem in terms of vectors and matrices is the first step toward solving some of the most complex and rewarding challenges in business and data science.

CONTINUE YOUR LEARNING

This chapter used several powerful NumPy functions to bring the concepts of linear algebra to life.

T summarizing the key vector/matrix manipulation tools.

TABLE 4-1: NumPy’s Manipulation Tools

FUNCTION NAME

NUMPY FUNCTION

DESCRIPTION

Dot product

np.dot(a, b)

Calculates the dot product of two vec-

tors or the product of two matrices.

Matrix multiplication

A @ b

A shorthand operator for matrix multi-

(shortcut)

plication (np.matmul).

Transpose

np.transpose(a) or a.T

Flips a matrix over its diagonal,

turning its rows into columns and its

columns into rows.

Array (creation)

np.array([...])

The fundamental function to create a

NumPy array (vector or matrix) from

a list.

Column stack

np.column_stack([...])

Takes a list of 1D vectors and stacks

them together as columns to form a

2D matrix.

Covariance

np.cov(m)

Calculates the covariance matrix,

showing how variables move together.

Continue Your Learning ❘ 81

TABLE 4-2: NumPy’s Linear Algebra Functions

FUNCTION NAME

NUMPY FUNCTION

DESCRIPTION

Vector norm (magnitude)

np.linalg.norm(a)

Calculates the L2 norm (Euclidean

length or magnitude) of a vector.

Eigenvalues/eigenvectors

np.linalg.eig(a)

Computes the eigenvalues and

eigenvectors of a square matrix.

Eigenvalues/eigenvectors

np.linalg.eigh(a)

A specialized, more stable version

(symmetric)

of eig for symmetric matrices (like a

covariance matrix).

Solve linear system

np.linalg.solve(A, b)

Solves a system of linear equations

in the form Ax = b.

Matrix inverse

np.linalg.inv(a)

Calculates the inverse of a square

matrix.

Find max index (arg max)

np.argmax(a)

Returns the index (not the value) of

the maximum element in an array.

Tile array (repeat)

np.tile(A, reps)

“Tiles” or repeats an array A a speci-

fied number of times.

In addition, while NumPy contains hundreds of functions, a handful are essential for day-to-day data analysis and linear algebra. T, which are split between NumPy’s main library and its specialized linalg (linear algebra) submodule.

5Calculus for Business Problem

Solving

From just living your daily life, you are probably already an expert in the study of change. In business, we track whether sales are rising or falling, if customer growth is accelerating, and when costs are starting to creep up. This constant motion is the lifeblood of any enterprise. But what if you had a precise mathematical language to describe, measure, and even predict these dynamics? That language is calculus.

In the business world, calculus is a practical toolkit for understanding the momentum of your operations. It’s the difference between knowing your company’s yearly revenue and knowing the exact rate at which that revenue was growing on the day you launched a new marketing campaign. It allows you to pinpoint the exact moment when your marketing efforts hit the point of diminishing returns, and it gives you a framework for modeling the entire lifecycle of a new product, from launch to market saturation.

This chapter demystifies calculus by putting it to work on real-world business problems using Python. It starts with common business data, like daily sales figures, and uses numerical calculus to find rates of change, acceleration, and total accumulation. The Python ecosystem is rich with tools to do calculus and so you’ll take a brief tour of the Python calculus ecosystem, from the numerical power of NumPy and SciPy to the symbolic capabilities of SymPy. From there, the chapter moves into forecasting, using differential equations to model growth curves. You’ll even tackle multi-variable problems by visualizing a “profit landscape” and exploring how to measure the impact of individual decisions. Finally, the chapter brings all these concepts together in a case study that uses marginal analysis to understand the dynamics of profitability.

By the end of this chapter, you’ll be equipped to use these powerful mathematical ideas in your Python code. You will move from simply observing data to actively analyzing the dynamics behind it, laying the foundation for making smarter, more data-driven business decisions.

84 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving NUMERICAL DIFFERENTIATION AND INTEGRATION IN

BUSINESS ANALYTICS

In a perfect textbook world, business trends would follow smooth, predictable curves that we could define with elegant functions. In reality, data is usually sparse and noisy. For example, consider a series of discrete sales measurements taken day by day or month by month. This is where the power of numerical calculus comes in. You can apply the core ideas of differentiation and integration directly to your data to uncover powerful insights about rates of change, pinpoint the exact moment of diminishing returns, and calculate total accumulation, all without needing a perfect formula. The following sections explore each of these concepts in detail: using the derivative to find the rate of change, the second derivative to find the point of diminishing returns, and the integral to accumulate totals.

The Derivative: Finding the Rate of Change

The derivative is simply a measurement of how a value is changing at a specific point in time. Think of it as the speedometer for your business. Your car’s main odometer tells you the total distance you’ve traveled (your cumulative sales), but it’s the speedometer that tells you how fast you’re going right now (your sales growth rate). This instantaneous speed is crucial for making timely decisions.

Consider this business question: You just launched a new mobile game, and you’re tracking the total number of downloads. Is the excitement for your game speeding up or slowing down? The total download count will always go up, but the derivative (the rate of new downloads per day) tells you about the project’s momentum.

In Python, you don’t need complex formulas to answer this question. When working with a sequence of data points (like daily sales figures), you can use NumPy’s diff() function to find the rate of change between consecutive data points. This gives you a practical, powerful way to see how the data is changing over time.

Imagine your game’s download numbers over its first 10 days. As shown in Listing 5-1, you can store this data as a NumPy array. Then you can use NumPy’s .diff() function to compute the difference.

LISTING 5-1: ANALYZING MOBILE GAME DOWNLOADS

import numpy as np

import matplotlib.pyplot as plt

# Daily cumulative downloads for the first 10 days

cumulative_downloads = np.array([0, 150, 400, 800, 1300, 1850, 2400, 2900, 3300, 3600])

# Calculate the daily new downloads using np.diff()

daily_new_downloads = np.diff(cumulative_downloads)

# Print the results

print(f"Cumulative Downloads: {cumulative_downloads}")

print(f"Daily New Downloads: {daily_new_downloads}")

numerical Differentiation and integration in Business Analytics ❘ 85

# --- Visualization ---

fig, ax1 = plt.subplots(figsize=(10, 6))

# Plot cumulative downloads on the primary y-axis (ax1)

color = 'tab:blue'

ax1.set_xlabel('Day')

ax1.set_ylabel('Total Downloads', color=color)

ax1.plot(cumulative_downloads, color=color, marker='o', line-

style='-', label='Cumulative Downloads')

ax1.tick_params(axis='y', labelcolor=color)

ax1.grid(True)

# Create a secondary y-axis (ax2) for the daily rate

ax2 = ax1.twinx()

color = 'tab:green'

ax2.set_ylabel('New Downloads per Day', color=color)

# We plot from day 1, as the rate is between days

ax2.plot(range(1, len(daily_new_downloads) + 1), daily_new_down-

loads, color=color, marker='s', linestyle='--', label='Daily New Downloads') ax2.tick_params(axis='y', labelcolor=color)

fig.suptitle('Mobile Game Download Momentum', fontsize=16)

fig.tight_layout()

plt.show()

Listing 5-1 starts by creating an array, cumulative_downloads, that holds the daily cumulative download values. In a real-world program, this data could be read from a file rather than hardcoded.

This data array is then passed to the NumPy .diff() function. This function computes the difference for the full array. It effectively subtracts Day 1 from Day 2, Day 2 from Day 3, and so on, for every column simultaneously. The computed value provides a new array holding the daily new download values. The results of these lines are then printed to the screen:

Cumulative Downloads: [0 150 400 800 1300 1850 2400 2900 3300 3600]

Daily New Downloads: [150 250 400 500 550 550 500 400 300]

After printing the values, This is done using Matplotlib’s twinx() feature, which allows you to have two different y-axes sharing the same x-axis (days).

First, you set up the primary y-axis (ax1) to plot the cumulative_downloads. Use a solid line (linestyle='-') with circular markers (marker='o') to represent the steady, upward trend of total downloads.

Next, you create a secondary y-axis (ax2 = ax1.twinx()) for the daily rate. This is crucial because the scale of daily new downloads (hundreds) is much smaller than the scale of cumulative downloads (thousands). If you plotted them on the same axis, the daily rate line would look flat and insignificant at the bottom of the chart. By giving it its own axis on the right side, you can see its true shape clearly. You then plot this daily_new_downloads data using a dashed line (linestyle='--') with square markers (marker='s') to distinguish it from the cumulative total. Note that since this is plotting the difference in value between two days, it will start on Day 1 instead of Day 0.

The visualization tells a clear story that the raw cumulative numbers hide. As you can see, even though the solid line (Total Downloads) is always rising, the green line (Daily New Downloads)

86 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving

Mobile Game Download Momentum

550

3500

500

3000

450

2500

400

2000

350

1500

300

Total Downloads

1000

New Downloads per Day

250

500

200

0

150

0

2

4

6

8

Day

FIGURE 5-1: Total number of mobile game downloads over time.

reveals the true momentum. The game’s growth accelerated rapidly for the first five days, peaked when daily downloads were growing at a rate of 550 downloads per day, and has been slowing down since Day 7. This is a critical insight. It tells you that your initial launch buzz is fading and now might be the perfect time for a new marketing push to reaccelerate growth.

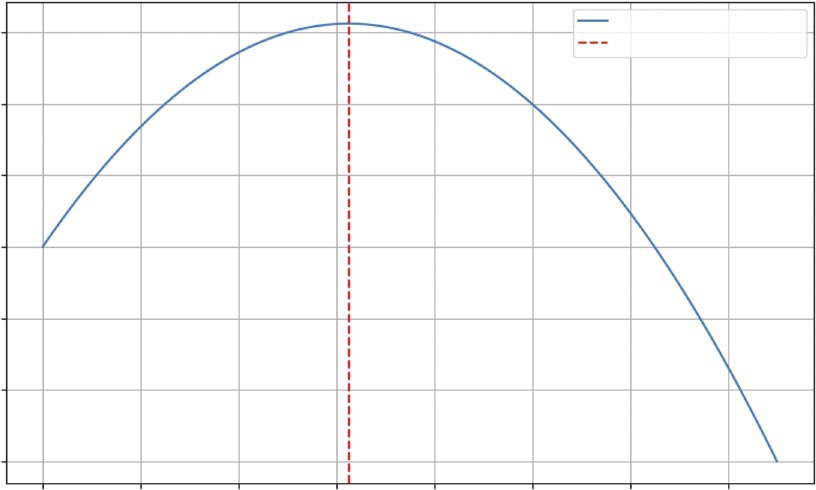

The Second Derivative: Pinpointing the Point of Diminishing

Returns

The second derivative measures the rate of change of the rate of change. It’s not the speed, but the acceleration of your metric. Its most powerful use in business is to find the inflection point—the precise moment when a trend’s momentum shifts. For a growing metric, this is the point of diminishing returns: the moment the growth begins to slow down.

To calculate this, you simply take the derivative of the first derivative. In NumPy, this means applying np.diff() a second time. Listing 5-2 uses the daily_new_downloads array calculated in the previous section and passes it through np.diff() again. This gives you a new array, called download_

acceleration, which represents the day-to-day change in the growth rate. Combine the code from Listing 5-1 and Listing 5-2.

LISTING 5-2: FINDING THE INFLECTION POINT FOR GAME DOWNLOADS

# The first derivative is the daily new downloads

daily_new_downloads = np.array([150, 250, 400, 500, 550, 550, 500, 400, 300])

numerical Differentiation and integration in Business Analytics ❘ 87

# The second derivative is the "acceleration" of downloads

download_acceleration = np.diff(daily_new_downloads)

print(f"Download Acceleration: {download_acceleration}")

# --- Visualization ---

plt.figure(figsize=(10, 6))

# Plot the first derivative (daily rate)

plt.plot(range(1, len(daily_new_downloads) + 1), daily_new_downloads, 'g-s', label='Daily New Downloads (1st Derivative)')

# Plot the second derivative (acceleration)

plt.plot(range(2, len(download_acceleration) + 2), download_acceleration, 'b-^', label='Download Acceleration (2nd Derivative)')

plt.axhline(y=0, color='grey', linestyle='--')

plt.title('Finding the Point of Diminishing Returns')

plt.xlabel('Day')

plt.ylabel('Change in Downloads')

plt.legend()

plt.grid(True)

plt.show()

The result:

Download Acceleration: [100 150 100 50 0 -50 -100 -100]

The visualization makes the story clear, The daily rate (squares) and the acceleration (triangles) are plotted on the same graph. Notice that there is also a horizontal dashed line at zero (plt.axhline(y=0)). This simple addition is crucial because it acts as a visual boundary.

The lower line (acceleration) shows the momentum. It’s positive for the first few days, meaning growth is speeding up. It’s zero on Day 6, and then it turns negative. Day 7, where the acceleration first becomes negative (−50), is the inflection point. This is the point of diminishing returns. Even though you still gained 500 new users on Day 7, the growth engine had started to slow down. For a business, this is the signal that a strategy (like an initial marketing blast) has reached its peak effectiveness and it’s time to consider a new approach to reaccelerate growth.

The Integral: Accumulating the Totals

Integration is the reverse of differentiation. If the derivative acts as a speedometer by converting the position function into velocity, the integral is the odometer that converts the velocity function into total distance traveled. It allows you to “sum up” a series of small, incremental changes to understand their cumulative impact.

This is incredibly useful in business. Imagine you know the number of new subscribers your streaming service gets each day. How do you find your total subscriber count at the end of the month, by using integration?

For numerical data, this process is wonderfully simple. You can use NumPy’s cumsum() function, which calculates the cumulative sum of an array. It takes a stream of rate data and returns the total accumulation over time.

88 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving

Finding the Point of Diminishing Returns

500

400

300

200

Change in Downloads 100

0

Daily New Downloads (1st Derivative)

–100

Download Acceleration (2nd Derivative)

1

2

3

4

5

6

7

8

9

Day

FIGURE 5-2: Visualization of the second derivative.

Say you have the daily numbers for new subscribers over a week. As shown in Listing 5-3, you can use cumsum() to see how the total user base grows.

LISTING 5-3: TRACKING STREAMING SERVICE SUBSCRIBERS

import numpy as np

import matplotlib.pyplot as plt

# Number of new subscribers each day for a week

daily_new_subs = np.array([120, 135, 150, 160, 145, 110, 90])

days = ['Mon', 'Tue', 'Wed', 'Thu', 'Fri', 'Sat', 'Sun']

# Calculate the cumulative sum of subscribers

total_subs = np.cumsum(daily_new_subs)

# Print the results

print(f"Daily New Subscribers: {daily_new_subs}")

print(f"Total Subscribers: {total_subs}")

# --- Visualization ---

plt.figure(figsize=(10, 6))

plt.bar(days, daily_new_subs, color='skyblue', label='New Subscribers Each Day')

numerical Differentiation and integration in Business Analytics ❘ 89

plt.plot(days, total_subs, color='navy', marker='o', linestyle='-',

label='Total Subscriber Count')

plt.title('Streaming Service Growth Over One Week')

plt.ylabel('Number of Subscribers')

plt.xlabel('Day of the Week')

plt.legend()

plt.grid(axis='y', linestyle='--', alpha=0.7)

plt.show()

This code starts with the daily_new_subs array. The calculation happens in the single line total_subs = np.cumsum(daily_new_subs). This function iterates through the array, keeping a running total. The first element is just 120. The second element is 120 + 135 = 255. The third is 120 + 135 + 150 = 405, and so on.

The results confirm this:

Daily New Subscribers: [120 135 150 160 145 110 90]

Total Subscribers: [120 255 405 565 710 820 910]

The visualization code then combines these two views. It uses plt.bar to show the daily rate as a light blue bar chart and plt.plot to overlay the cumulative total as a dark navy line chart. The

It clearly shows how the daily rate (the bar chart) directly builds the Streaming Service Growth Over One Week

Total Subscriber Count

New Subscribers Each Day

800

600

400

Number of Subscribers

200

0

Mon

Tue

Wed

Thu

Fri

Sat

Sun

Day of the Week

FIGURE 5-3: Demonstration of integration using subscriber growth.

90 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving cumulative total (the line chart). You can see that the subscriber acquisition peaked mid-week on Thursday and slowed over the weekend. By the end of the week, those daily gains accumulated to a total of 910 new subscribers. This simple act of integration gives you a complete picture of the daily performance and its overall impact.

THE CALCULUS ECOSYSTEM IN PYTHON

So far, this chapter has focused on the numerical approach to calculus using NumPy, which is perfect when your starting point is a collection of data points. However, the Python ecosystem offers a rich set of tools for different kinds of calculus problems. There are several main approaches, which include numerical calculus, symbolic calculus, and advanced numerical methods.

The following subsections take a brief look at each of these approaches. The discussion starts with numerical calculus using NumPy for analyzing array data. Then, you’ll explore symbolic calculus with SymPy for working directly with mathematical formulas. Finally, you’ll learn a bit about advanced numerical methods using SciPy for high-precision tasks like integration.

Numerical Calculus with NumPy

Numerical calculus using NumPy is the method you’ve been using. It’s the best choice when you have data in an array and want to find the differences between points (np.diff) or the cumulative sum (np.cumsum). It’s fast, efficient, and direct for data analysis.

As an example, imagine a matrix where each row represents a day and each column represents a different product. The values are the cumulative sales for that product. As shown in Listing 5-4, you can use np.diff to find the daily new sales for all products at once.

LISTING 5-4: DIFFERENTIATING A SALES MATRIX

import numpy as np

# Cumulative sales matrix: 4 days, 3 products

# Product A, Product B, Product C

sales_matrix = np.array([

[100, 50, 200], # Day 1

[110, 55, 215], # Day 2

[125, 65, 235], # Day 3

[145, 80, 250] # Day 4

])

# Differentiate along the rows (axis=0) to get daily changes

daily_sales_growth = np.diff(sales_matrix, axis=0)

print("--- Daily Sales Growth ---")

print(daily_sales_growth)

The Calculus Ecosystem in Python ❘ 91

This example first defines a matrix (sales_matrix) that contains the sales for three products over four days. The key line is daily_sales_growth = np.diff(sales_matrix, axis=0). By specifying axis=0, you tell NumPy to perform the difference operation along the rows (vertically). The output matrix shows the new sales each day for each product:

--- Daily Sales Growth ---

[[10 5 15]

[15 10 20]

[20 15 15]]

For instance, on the second day (the first row of the output), Product A sold 10 new units (110 − 100), Product B sold 5 (55 − 50), and Product C sold 15 (215 − 200).

Symbolic Calculus with SymPy

What if you don’t have data, but a mathematical formula? For example, you might have a cost function C(x) = 0.01x2 + 50x + 5,000. If you want to find the derivative or integral of the formula itself, you need a symbolic math library.

SymPy is the standard for this in Python. It works with abstract symbols, not numbers, to give you exact analytical results. Listing 5-5 uses SymPy for a cost function.

LISTING 5-5: USING SYMPY FOR A COST FUNCTION

import sympy as sp

# 1. Define 'x' as a mathematical symbol

x = sp.symbols('x')

# 2. Create a symbolic expression for our cost function

cost_function = 0.01*x**2 + 50*x + 5000

# 3. Calculate the derivative (marginal cost function)

marginal_cost_function = sp.diff(cost_function, x)

# 4. Calculate the integral (if we wanted to reverse the process)

integral_of_cost = sp.integrate(cost_function, x)

print(f"Original Cost Function: {cost_function}")

print(f"Marginal Cost Function: {marginal_cost_function}")

print(f"Integral of Cost Function: {integral_of_cost}")

The code first defines x as an abstract symbol using sp.symbols('x'). This tells Python to treat x not as a variable holding a specific number, but as a mathematical placeholder, allowing you to build the cost_function as a symbolic expression.

Once you have this expression, you use SymPy’s core calculus functions. sp.diff(cost_function, x) takes the expression and calculates its exact derivative with respect to x, giving the marginal cost function.

92 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving Conversely, sp.integrate(cost_function, x) finds the indefinite integral of the expression, effectively reversing the differentiation process.

The output confirms that SymPy has performed these symbolic manipulations correctly: Original Cost Function: 0.01*x**2 + 50*x + 5000

Marginal Cost Function: 0.02*x + 50

Integral of Cost Function: 0.00333333333333333*x**3 + 25.0*x**2 + 5000.0*x The code determined the derivative of the cost function, which represents the marginal cost. It also found the indefinite integral, reversing the operation. Notice that the integral includes a term, showing how it recovered the original structure from the constant term in your cost function.

Advanced Numerical Methods with SciPy

While NumPy provides the basics, SciPy provides a library of more advanced, high-performance numerical routines. When it comes to calculus, its scipy.integrate module is essential. You will see how to use solve_ivp later in this chapter to solve differential equations. Another key function is quad, which can find the definite integral of any Python function with high precision.

Let’s say you have a Python function that represents your marginal revenue. You can use scipy.

integrate.quad to find the total revenue gained by selling a certain range of products for instance, from the 100th unit to the 500th unit. Listing 5-6 shows an example of using the quad function.

LISTING 5-6: USING SCIPY TO INTEGRATE A FUNCTION

from scipy import integrate

# Our marginal revenue function: MR = 100 - 0.1*q

def marginal_revenue(q):

return 100 - 0.1 * q

# Integrate the function from quantity=100 to quantity=500

# The 'quad' function returns the result and an estimate of the error total_revenue_gained, error = integrate.quad(marginal_revenue, 100, 500) print(f"Total revenue from selling units 100 to 500: ${total_revenue_gained:.2f}") print(f"Estimated error of the calculation: {error}")

The integrate.quad() function takes three main arguments: the function you want to integrate (marginal_revenue) and the start and end points of the integration interval (100 and 500). It returns two values: the calculated integral and an estimate of the absolute error.

The output from this listing is as follows:

Total revenue from selling units 100 to 500: $34000.00

Estimated error of the calculation: 3.774758283725532e-13

Solving Business growth and Pricing models with Differential Equations ❘ 93

The extremely small error value indicates that the total revenue figure of $34,000.00 is highly precise.

The quad function is the go-to tool when you need a precise numerical integral of a Python function.

Choosing the Right Tool

You can clearly see that Python can solve any problem. Which tool is the right one depends on your problem. The following can serve as a guide for what tool to use when:

➤

Starting with a spreadsheet or data array? Use NumPy.

➤

Starting with a mathematical formula? Use SymPy.

➤

Need to solve a differential equation or find a high-precision integral of a function? Use SciPy.

SOLVING BUSINESS GROWTH AND PRICING MODELS WITH

DIFFERENTIAL EQUATIONS

While analyzing historical data is essential, the ultimate goal for many businesses is to look into the future. Businesses need to build models that can forecast growth, predict market saturation, and understand how systems evolve over time. This is the domain of differential equations.

If you think of the previous examples as reading a ship’s log to see where it has been, think of differential equations as using the ship’s current speed and the ocean currents to chart its future course.

A differential equation is a powerful rule or “recipe” that describes how a system changes, where the rate of change depends on the current state of the system.

This concept is at the heart of many business dynamics:

➤

Viral marketing: The rate of new sign-ups is proportional to the number of existing users who can share the product. More users equals faster growth.

➤

Compound interest: The rate at which your investment grows is proportional to the current balance. More money equals faster earnings.

➤

Product adoption: The rate of new customers often depends on how many potential customers are left in the market. As the market becomes saturated, growth naturally slows down.

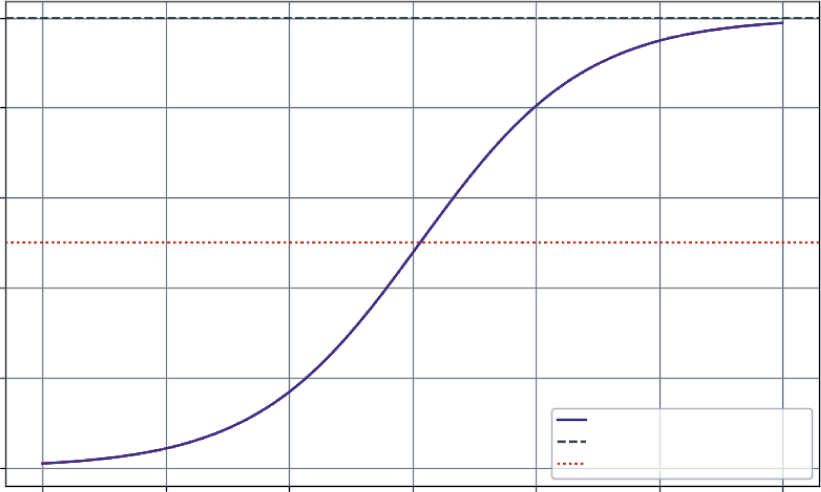

The example of product adoption is famously modeled by the logistic growth curve (or S-curve), which describes the lifecycle of many products and services: a slow start, a period of rapid growth, and a final leveling-off as the market capacity is reached.

To solve these models and generate forecasts in Python, you can use a powerful tool from the SciPy library: solve_ivp (Solve Initial Value Problem). You simply provide the solve_ivp function with a starting point (your initial number of users), a function that defines your “recipe for growth,” and a time frame. It does the hard work of simulating the system’s evolution.

94 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving As an example, consider the growth of a new streaming service. You have 100 beta testers at launch.

Based on market research, your company believes the total potential market is 10,000 subscribers.

You want to project subscriber growth over the next three years.

The “recipe for growth” is the logistic model, which states that the growth rate is proportional to both the current number of users and the remaining market space. Listing 5-7 contains code for modeling this.

LISTING 5-7: MODELING A SUBSCRIPTION SERVICE’S GROWTH

import numpy as np

from scipy.integrate import solve_ivp

import matplotlib.pyplot as plt

# --- 1. Define the Model Parameters ---

P0 = 100 # Initial number of subscribers

K = 10000 # Market capacity (carrying capacity)

r = 1.5 # Intrinsic growth rate (e.g., 150% per year)

# --- 2. Define the Differential Equation (The "Recipe") ---

# This function describes the rate of change at any given time t and population P

def logistic_growth(t, P):

# The logistic equation: dP/dt = r * P * (1 - P/K)

return r * P * (1 - P / K)

# --- 3. Set up and Run the Solver ---

# Time span: 0 to 3 years

t_span = [0, 6]

# Points in time where we want the solution

t_eval = np.linspace(t_span[0], t_span[1], 100)

# Use solve_ivp to get the solution

sol = solve_ivp(

fun=logistic_growth,

t_span=t_span,

y0=[P0],

t_eval=t_eval

)

Let’s break down how solve_ivp works. It’s a sophisticated numerical solver that you set up by passing it four key arguments:

➤

fun, which is your recipe, the logistic_growth function you define to tell the solver how to calculate the rate of change at any given moment.

➤

t_span, the start and end times for your simulation, [0, 6] years.

➤

y0, the starting state of your system, which is the initial 100 subscribers ([P0]).

Solving Business growth and Pricing models with Differential Equations ❘ 95

➤

t_eval, an optional but useful argument that tells the solver exactly which points in time you want it to report back.

This example asks for 100 evenly spaced points over the six years to ensure you get a smooth curve for plotting.

Under the hood, solve_ivp starts at P0 and takes a tiny step forward in time. It uses the function to calculate the growth rate, estimates the new subscriber count, and then repeats this process thousands of times. By stitching together these incremental steps, it accurately simulates the continuous growth curve without having to solve the complex differential equation by hand.

To better see what is happening, you can plot the results to see a graph of the results. Combine the code presented in Listing 5-8 with the code in Listing 5-7.

LISTING 5-8: VISUALIZING THE RESULTS OF THE SUBSCRIPTION SERVICE’S GROWTH

# --- 4. Visualize the Results ---

plt.figure(figsize=(10, 6))

plt.plot(sol.t, sol.y[0], label='Projected Subscriber Growth', color='purple') plt.axhline(y=K, color='grey', linestyle='--', label=f'Market Capacity ({K})') plt.axhline(y=K/2, color='red', linestyle=':', label='Point of Max Growth') plt.title('Subscription Service Growth Projection (S-Curve)')

plt.xlabel('Years')

plt.ylabel('Number of Subscribers')

plt.legend()

plt.grid(True)

plt.show()

The output, is a classic S-curve that provides a rich, strategic forecast for the business. Looking at the figure, you can see the following:

➤

Slow start (Year 0–2): In the first year, growth is modest as the service finds its footing with early adopters.

➤

Rapid growth (Year 2–4): As word-of-mouth and marketing kick in, the service enters a period of exponential growth. The rate of new subscribers is at its highest when you have half the market (the dotted line), as there’s a perfect balance of existing users to spread the word and new customers to acquire.

➤

Saturation (Year 4–6): As the service captures a majority of the potential market, growth slows significantly. It becomes harder and more expensive to find new subscribers.

This single model, born from a simple differential equation, is a powerful strategic roadmap. It helps you anticipate when to ramp up server capacity, when to shift marketing from acquisition to retention, and how to set realistic growth targets for investors.

96 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving

Subscription Service Growth Projection (S-curve)

10000

8000

6000

4000

Number of Subscribers

2000

Projected Subscriber Growth

Market Capacity (10000)

0

Point of Max Growth

0

1

2

3

4

5

6

Years

FIGURE 5-4: Subscription service growth project figure.

SENSITIVITY ANALYSIS WITH PARTIAL DERIVATIVES

In business, decisions are rarely made in a vacuum. A product’s profit doesn’t just depend on its price; it’s also affected by your marketing budget, production costs, and competitor actions. This chapter has been looking at how one variable changes another, but the real world is a landscape of interconnected factors. Partial derivatives are the tool you use to navigate this landscape.

A partial derivative lets you measure the rate of change of a function with respect to one variable, while holding all other variables constant. It answers crucial “what-if” questions at the heart of business strategy:

➤

“If we keep our ad spend the same, how will a $1 price increase affect our profit?”

➤

“Holding our price steady, what is the exact return on the next dollar we put into marketing?”

This is like standing on a hillside—the slope depends on the direction you’re facing. The partial derivative tells you the steepness if you decide to walk only east, or only north.

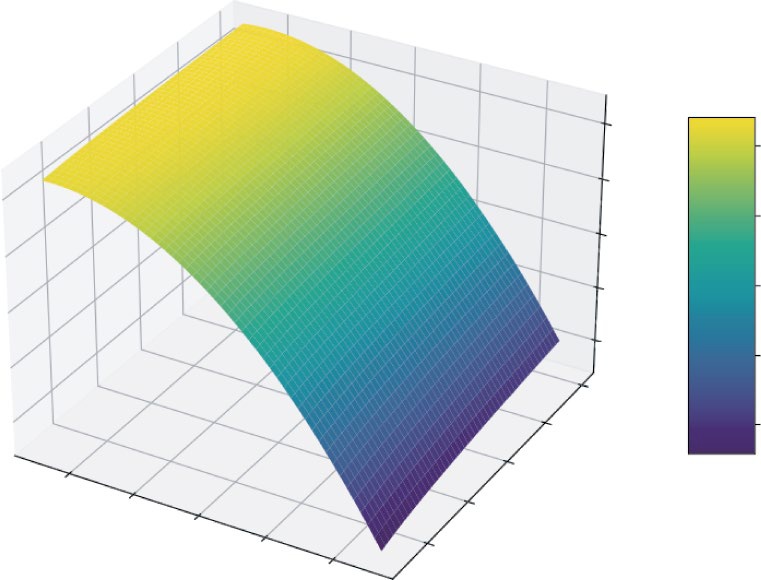

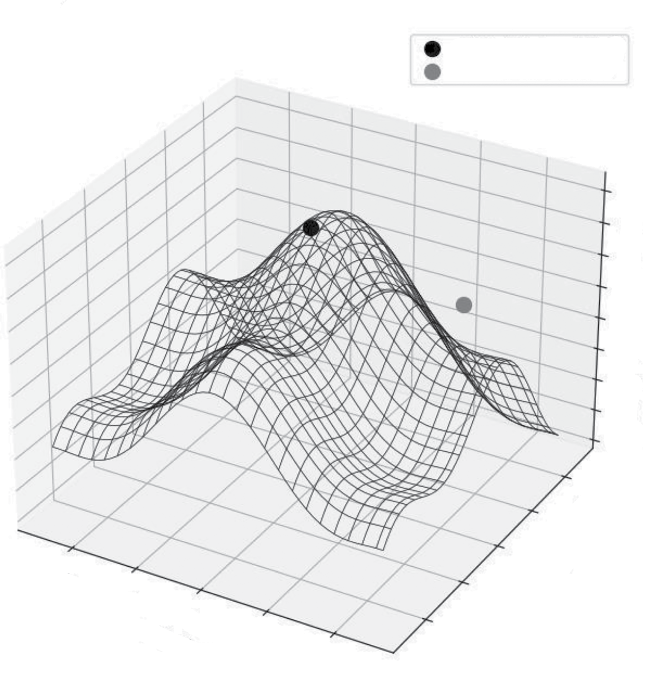

This next example models the profit for an online course. The profit depends on two key levers you control: the price of the course and your monthly marketing spend. Listing 5-9 presents a model of this and visualizes it as a 3D “profit surface” to see how these decisions interact.

Sensitivity Analysis with Partial Derivatives ❘ 97

LISTING 5-9: VISUALIZING A PROFIT LANDSCAPE

import numpy as np

import matplotlib.pyplot as plt

# Define a profit function with two variables

def calculate_profit(price, marketing_spend):

# Model how price affects quantity sold (higher price -> fewer sales) quantity_sold = 1000 - 10 * price + 2 * np.sqrt(marketing_spend)

# Model revenue

revenue = quantity_sold * price

# Model cost

cost = 2000 + (0.5 * marketing_spend) # Fixed cost + marketing

return revenue - cost

# --- Create a Grid of Inputs ---

# Generate a range of possible prices and marketing spends

price_range = np.linspace(50, 150, 50)

marketing_range = np.linspace(500, 5000, 50)

# np.meshgrid creates a coordinate grid from our two arrays

P, M = np.meshgrid(price_range, marketing_range)

# --- Calculate Profit Across the Grid ---

Z_profit = calculate_profit(P, M)

# --- Visualize the Profit Surface ---

fig = plt.figure(figsize=(12, 8))

ax = fig.add_subplot(111, projection='3d')

surf = ax.plot_surface(P, M, Z_profit, cmap='viridis', edgecolor='none') ax.set_title('Profit Landscape')

ax.set_xlabel('Price ($)')

ax.set_ylabel('Marketing Spend ($)')

ax.set_zlabel('Profit ($)')

fig.colorbar(surf, shrink=0.5, aspect=5, label='Profit')

plt.show()

Listing 5-9 first defines a calculate_profit function that takes price and marketing_spend as inputs. It models a realistic scenario where higher prices reduce sales quantity, while higher marketing spend increases it (but with diminishing returns, modeled by np.sqrt).

To visualize this, you need to calculate profit for many different combinations of price and marketing. np.linspace is used to create ranges of 50 evenly spaced values for both price and marketing.

Then, np.meshgrid combines these two 1D arrays into a 2D grid of coordinates. This grid represents every possible combination of price and marketing spend to test.

You then pass these entire grids, P and M, to the profit function, which returns Z_profit, a matrix containing the profit for every point on that grid. Finally, you use Matplotlib’s 3D plotting capabilities to render this as a surface.

98 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving

Profit Landscape

20000

20000

0

0

–20000

Profit ($)

–40000

–20000

Profit

–60000

–40000

5000

–60000

4000

3000

60

80

2000

100

Price ($)

120

1000

Marketing Spend ($)

140

FIGURE 5-5: 3D plot of the profit landscape.

This plot shows an intuitive feel for the profit landscape. You can see there’s a “ridge” where profit is maximized. If you set the price too high or too low, your profit falls off. Similarly, there are diminishing returns to marketing spend. This visualization turns a complex, two-variable problem into an intuitive map. A partial derivative at any point on this surface would tell you the slope in the direction of either the “Price” axis or the “Marketing Spend” axis, giving you a precise measurement of that variable’s impact.

CASE STUDY: REVENUE, COST, AND PROFIT ANALYSIS

This case study brings everything together. You’ve seen how derivatives reveal rates of change and integrals accumulate totals. Now, you’ll see how to apply these concepts to one of the most fundamental tasks in business: analyzing profitability.

In this case study, you’ll act as an analyst for a company launching a new product. You have data on production costs and a model for market demand. The goal isn’t to find the single “best” price (I save that for the next chapter on optimization), but to understand the dynamics of profit. Where does it grow fastest? When does producing one more unit stop being as profitable?

Case Study: Revenue, Cost, and Profit Analysis ❘ 99

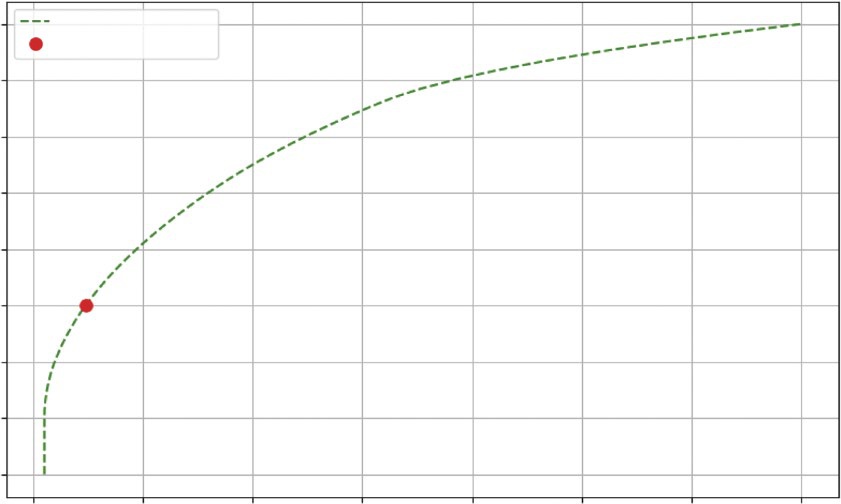

Step 1: Understanding Marginal Cost (the Derivative of Cost)

Your production team has given you a table of total costs for different production levels. As you produce more, you expect costs to rise, but due to economies of scale, they might not rise at a constant rate. The key metric you need to uncover is the marginal cost: the cost of producing one more unit. This is the derivative of the total cost. Using the code in Listing 5-10, you can uncover the margin cost.

LISTING 5-10: UNCOVERING THE MARGINAL COST

import numpy as np

import matplotlib.pyplot as plt

# Production levels from 0 to 1000 units, in steps of 100

quantity = np.arange(0, 1001, 100)

# Total cost to produce at each level (includes fixed costs + variable costs)

# Let's model this with a function for simplicity

fixed_cost = 5000

variable_cost_per_unit = 50

# Add a non-linear term to represent economies of scale

total_cost = fixed_cost + (variable_cost_per_unit * quantity) -

(0.01 * quantity**2)

# Calculate Marginal Cost using the derivative (np.diff)

# We divide by the change in quantity (100) to get the per-unit cost

marginal_cost = np.diff(total_cost) / np.diff(quantity)

# --- Visualization ---

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

# Plot Total Cost

ax1.plot(quantity, total_cost, 'b-o', label='Total Cost')

ax1.set_title('Total Production Cost')

ax1.set_xlabel('Quantity Produced')

ax1.set_ylabel('Cost ($)')

ax1.grid(True)

# Plot Marginal Cost

# We plot this at the midpoint of each interval

ax2.plot(quantity[1:], marginal_cost, 'g-s', label='Marginal Cost')

ax2.set_title('Marginal Cost per Unit')

ax2.set_xlabel('Quantity Produced')

ax2.set_ylabel('Cost per Additional Unit ($)')

ax2.grid(True)

plt.tight_layout()

plt.show()

This listing first creates the data. quantity is an array representing production levels from 0 to 1,000

in steps of 100. You then model total_cost using a formula that includes a fixed cost, a variable

100 ❘ CHAPTER 5 CAlCuluS foR BuSinESS PRoBlEm Solving

Total Production Cost

Marginal Cost per Unit

45000

47.5

40000

45.0

35000

30000

42.5

25000

40.0

Cost ($)

20000

37.5

15000

Cost per Additional Unit ($) 35.0

10000

32.5

5000

0

200

400

600

800

1000

200

400

600

800

1000

Quantity Produced

Quantity Produced

FIGURE 5-6: Total production cost and marginal cost per unit.

cost, and a small negative quadratic term (-0.01 * quantity**2) to simulate economies of scale, where costs rise a bit slower as quantity increases.

The crucial step is calculating the marginal_cost. The code uses np.diff(total_cost) to find the change in cost between each production level. However, since the production levels change by 100

units at a time (not 1), you must divide this by np.diff(quantity) (which is 100) to get the true per-unit marginal cost.

The visualization code then creates two side-by-side charts (using plt.subplots(1, 2)) to compare two views of this data,

you can see that the left chart shows the total cost, which always goes up.

The right chart, however, provides a deeper insight. The marginal cost is decreasing. For the first 100

units, each additional item costs about $49 to make. By the time you’re producing 1,000 units, the cost for just one more has dropped to $31. This is a classic sign of economies of scale: production is getting more efficient at higher volumes.

Step 2: Understanding Marginal Revenue (the Derivative of

Revenue)

Next, your marketing team provides a demand curve. They estimate that to sell more units, you need to lower the price. Total revenue is simply price * quantity. But you’re interested in the marginal revenue: the extra revenue you get from selling one more unit. The marginal revenue is computed in Listing 5-11.

Case Study: Revenue, Cost, and Profit Analysis ❘ 101

LISTING 5-11: COMPUTING MARGINAL AND TOTAL REVENUE